What has long been a notorious system finally gets a much-needed overhaul. Starting in 2026, Brazil is adopting a ‘best practice’, value-added tax framework with benefits that go beyond its intended purpose of simplification, efficiency, and compliance.

As most international accountants, finance professionals, and even ERP consultants will testify to, Brazil’s current tax system is among the most complex in the world. According to the World Bank, Brazil’s tax system ranks first worldwide in time spent on tax compliance, averaging 1,500 hours per year. By comparison, the next country on the list spends on average just over 1,000 hours per year, and countries such as Germany (218 hours) and the United States (175 hours) perform significantly better.

Change came in December 2023, when Brazil approved a constitutional amendment introducing a complete overhaul of its tax system.

A notoriously difficult tax regime

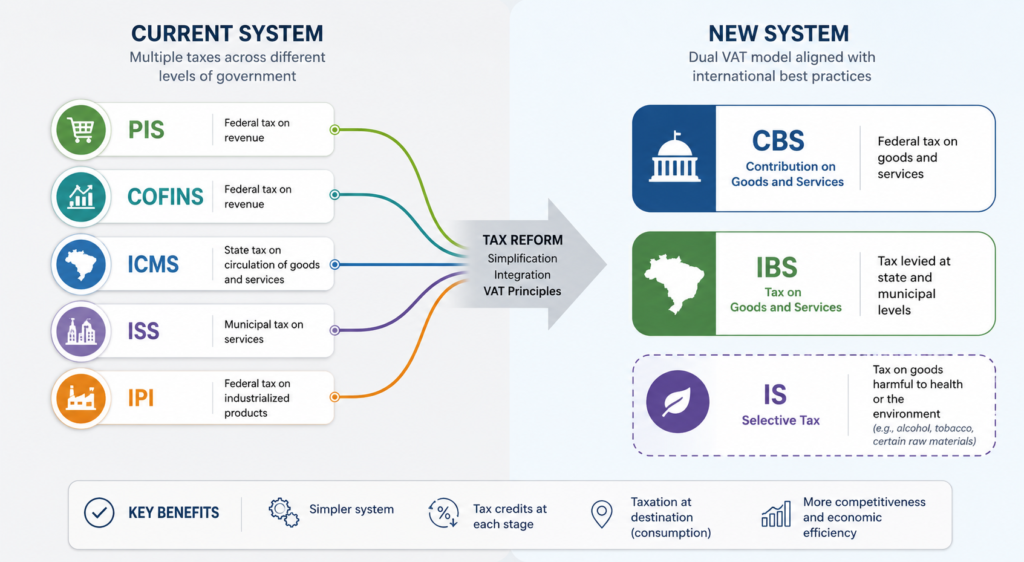

The origins of Brazil’s current system lie in the fragmented allocation of tax authority between the federal, state and municipal authorities. Each maintained its own interpretations, (reporting) rules, collection methods, forms and software systems. Taxation on goods would take place at both origin and destination, exceptions were widespread and cumulative and non-cumulative regimes varied by state and industry.

As the individual states within the federation started competing with each other by incentivising and exempting (“guerra fiscal”) complications only increased, leading to thousands of different rules, exceptions and regimes. A typical example of this system is the use of ‘ghost’ warehouses in certain states, established solely to reroute goods in order to benefit from local tax incentives.

Economists and business leaders coined the term ‘Custo Brasil’, or the so-called ‘Brazil Cost’. It refers to the additional costs embedded in goods and services, as well as the inefficiencies weighing on the economy caused by tax complexity, bureaucracy and regulatory burdens. Changing the system is expected to reduce the Custo Brasil, increase productivity, stimulate economic growth and attract foreign investment.

The Dual VAT system does just that – and more.

Best-practice VAT and destination principle

The reform introduces a new model that more closely resembles the value-added tax (VAT) systems used in many other countries.

It consists of two main components:

- CBS (Contribution on Goods and Services) – a federal tax on goods and services

- IBS (Tax on Goods and Services) – a tax levied at the combined state and municipal level

Together, these taxes will replace the existing consumption taxes. In addition, a selective tax (IS) will be introduced for goods considered harmful to health or the environment, such as alcohol and tobacco.

As illustrated above, the new framework consolidates several existing consumption taxes into two main components: CBS, a federal tax on goods and services, and IBS, a combined state and municipal consumption tax.

One of the most significant changes is the shift in taxation from the place of production to the place of consumption. Under the current system, taxes are generated throughout the production and distribution chain, encouraging states to attract manufacturing activity and distribution centres through local tax incentives, often at the expense of consumption-heavy regions.

Beyond simplification, efficiency and international standardisation, the reform therefore also represents a structural redistribution of tax revenues between Brazilian states. Under the new VAT-based model, tax revenues will primarily accrue where final consumption takes place rather than where production occurs.

Revamped credit system

The new system also introduces a far broader and more transparent tax credit mechanism. Under the current regime, companies often face restrictions, overlapping rules and legal uncertainty when recovering indirect taxes paid throughout the supply chain, with credit entitlement frequently varying by tax type, state and industry.

Under the new VAT-based framework, businesses will generally be able to claim tax credits on taxes paid on goods and services acquired as inputs to their economic activity. This non-cumulative model is intended to reduce “tax cascading” — the compounding effect of taxes being applied on top of previously taxed amounts throughout the production chain.

As a result, tax costs should become more neutral and predictable, particularly for foreign companies operating in Brazil or managing cross-state supply chains. The reform is expected to reduce distortions between sectors, improve transparency and create a more internationally recognisable tax environment for investors and multinational businesses.

Phased transition

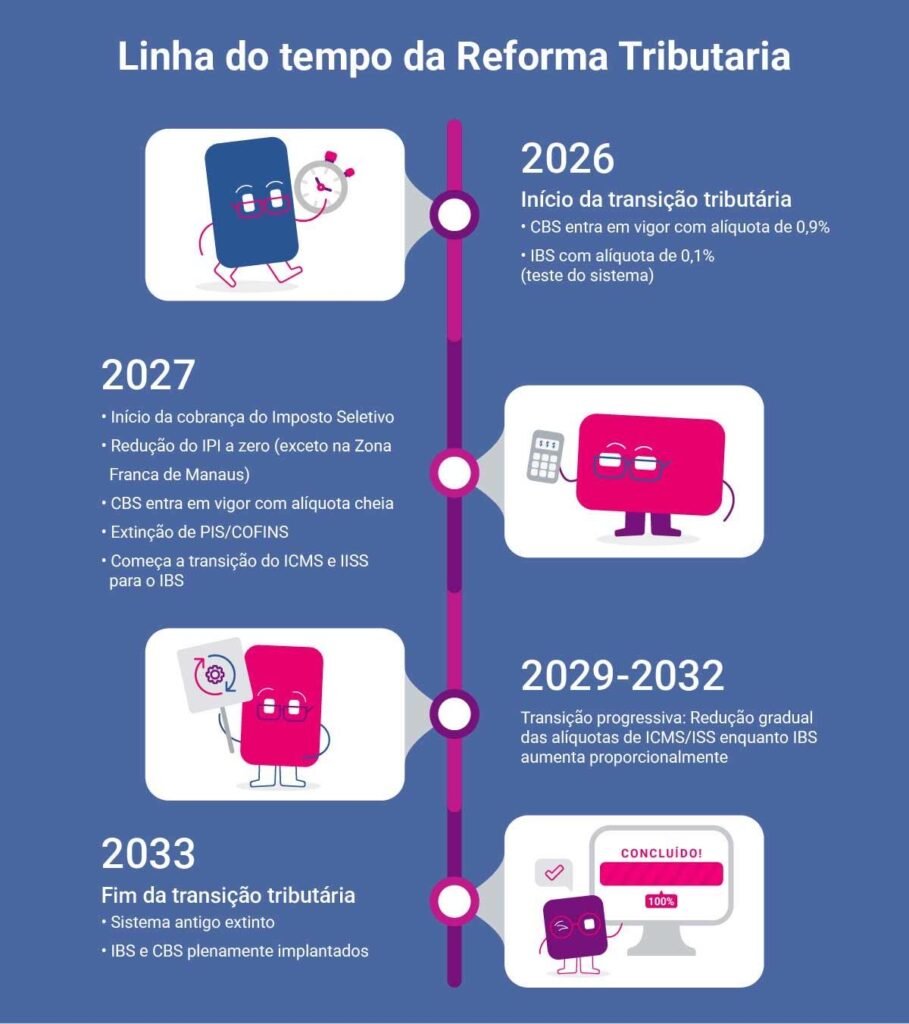

While the new tax framework promises significant simplification in the long term, the transition period will initially increase complexity for businesses operating in Brazil. Rather than replacing the existing system overnight, the reform will be implemented gradually between 2026 and 2033, with old and new taxes operating in parallel for several years.

Beginning in 2026, CBS and IBS will be introduced at reduced test rates alongside the current regime. Over the following years, the existing consumption taxes — including PIS, COFINS, ICMS, ISS and IPI — will gradually be reduced and phased out, while the new VAT-based taxes increase proportionally. Full implementation of the new system is currently scheduled for 2033.

For foreign companies, multinationals and investors, readiness during this transition phase will be critical. Businesses will need to adapt ERP systems, invoicing structures, tax determination logic, reporting processes and supply chain models to accommodate both tax regimes simultaneously. Contract structures, pricing models and tax credit recovery processes may also require reassessment.

The transition period therefore represents not only a compliance challenge, but also a strategic opportunity. Companies that prepare early will be better positioned to reduce operational disruption, optimise tax recovery and adapt more efficiently to Brazil’s new consumption tax environment.

Economic impact and business outlook

For Brazil as a whole, the reform represents far more than a technical tax overhaul. By replacing one of the world’s most fragmented and administratively burdensome tax systems with a more modern VAT structure, the country is aiming to reduce inefficiency across virtually every layer of the economy.

Part of that impact will come from a gradual redistribution of tax revenues between Brazilian states. Under the new model, tax income will increasingly flow toward the states where goods and services are actually consumed, rather than where production or distribution is artificially concentrated for tax purposes. Over time, this is expected to reduce some of the economic distortions created by decades of state-level tax competition and incentive structures.

More importantly however, the reform is designed to improve the overall efficiency of the Brazilian economy. Lower compliance costs, fewer cascading taxes, greater transparency and more predictable tax treatment should make it easier for businesses to operate, expand and invest across state borders. For a country long associated with the administrative burden of the “Custo Brasil”, this alone could become one of the reform’s most significant achievements.

For foreign investors and international businesses, the changes may make Brazil a considerably more accessible market over the coming years. While the transition period will require preparation and system adjustments, the long-term direction is toward a tax environment that is more aligned with international standards and easier to understand for multinational organisations.

In practical terms, companies may benefit from simpler supply chain structures, more transparent tax recovery mechanisms and reduced operational friction when doing business across different regions of Brazil. For many international businesses, the reform could ultimately lower one of the largest historical barriers to operating in the Brazilian market.

Conclusion

Brazil’s tax reform marks one of the country’s most significant economic modernisation efforts in decades. By replacing a fragmented and highly complex tax structure with a more transparent dual-VAT system, Brazil is moving toward a framework that is more efficient, predictable and aligned with international standards.

The transition period between 2026 and 2033 will inevitably bring challenges, particularly for businesses required to operate under parallel tax regimes while adapting systems, processes and supply chains. Readiness during this phase will be essential.

In the long term however, the reform has the potential to significantly reduce the administrative burden associated with the “Custo Brasil”, improve economic efficiency and create a more accessible business environment for both domestic and international companies. For foreign investors in particular, the direction is clear: Brazil is becoming easier to understand, easier to operate in and increasingly aligned with the global tax landscape.